Beyond the Sprawl: A Mathematical Fix for Ontario’s Housing Viability Crisis

Table of contents

Step-by-Step Legal Protocol for LTB Non-Payment

- The "Supply Myth" and the Great Decoupling

- The Core Framework: The Viability Gap Matrix

- The "Unsexy" Solutions: Three Levers to Fix the Pro-Forma

- The "War Story" (Case Study): A Stalled Condo in Mississauga

- Conclusion: The Mathematics of Momentum

- Checklist for the Ministry of Municipal Affairs and Housing

Get in touch with our team at Zulma Real Estate and let's build something that works.

The political fixation on building 1.5 million homes in Ontario has become a dangerous distraction. It is a slogan masquerading as a strategy, built on the flawed premise that the primary obstacle to housing supply remains regulatory red tape and municipal intransigence. While streamlining the approvals process - from glacial Site Plan Approval timelines to the capricious nature of the Committee of Adjustment - remains necessary, it is no longer the binding constraint.

We have spent the last several years aggressively dismantling zoning barriers, increasing allowable Floor Space Index (FSI) near transit corridors, and attempting to curb the influence of NIMBY appeals at the Ontario Land Tribunal (OLT). Provincial legislation, culminating in the recent Fighting Delays, Building Faster Act, 2025 (Bill 60), has prioritized supply enablement.

Yet, the data emerging in late 2025 tells a starkly different story. Housing starts across the Greater Toronto Area (GTA) and the extended Golden Horseshoe are not accelerating; they are decelerating, rapidly approaching decade lows.

The reason is simple, yet persistently ignored in political discourse: the mathematics of development no longer work. The pro-forma is broken.

After twenty years navigating the intersection of CMHC policy, municipal planning boards, and private equity deployment in the GTA, the reality on the ground is clear. This is not a supply crisis; it is a viability crisis. We do not lack land, nor do we lack ambition. We lack projects that can secure financing in the current economic environment. The decoupling of construction costs and market reality has rendered the vast majority of zoned density financially inert.

The "Supply Myth" and the Great Decoupling

The assumption underpinning the current provincial strategy is that if we reduce regulatory barriers, the free market will inherently deliver the required housing stock. This logic held true in a low-interest-rate environment where asset appreciation consistently outpaced construction cost inflation. It fails spectacularly in the current economic climate.

We are witnessing a simultaneous shock to both the numerator and the denominator of the development equation.

On the cost side, construction hard costs which is driven by acute skilled labour shortages, supply chain volatility, and material inflation have surged by over 40% since 2020. This is not cyclical inflation; it is a structural shift in the cost of delivering high-density housing.

On the revenue side, purchasing power has collapsed. The Bank of Canada’s necessary, albeit painful, tightening cycle has driven mortgage qualification rates to levels that fundamentally disconnect from current asset prices. The benchmark home price in Ontario, having corrected to approximately $859,000 (down 20% from the peak), remains agonizingly out of reach for the median income household. A family that qualified for an $800,000 mortgage three years ago may only qualify for $600,000 today.

The fallout is most visible in the condominium pre-sale market, the traditional engine of housing finance in Ontario. Pre-sales have evaporated. Investors, who previously comprised 50-60% of pre-sale buyers, cannot achieve positive cash flow at current interest rates. End-users are paralyzed by uncertainty and qualification hurdles. Without the 70-80% pre-sale coverage required by lenders, construction financing, the lifeblood of new supply is simply unavailable.

While Purpose-Built Rental (PBR) completions are currently high, this is largely a lagging indicator, reflecting projects initiated during a lower-rate environment. The pipeline for new PBR starts is beginning to face the same viability challenges.

If Ontario is serious about restarting the engine of housing supply, we must move beyond the rhetoric of "cutting red tape" and address the core economic factors stalling development. We need a technical roadmap focused on bridging the viability gap.

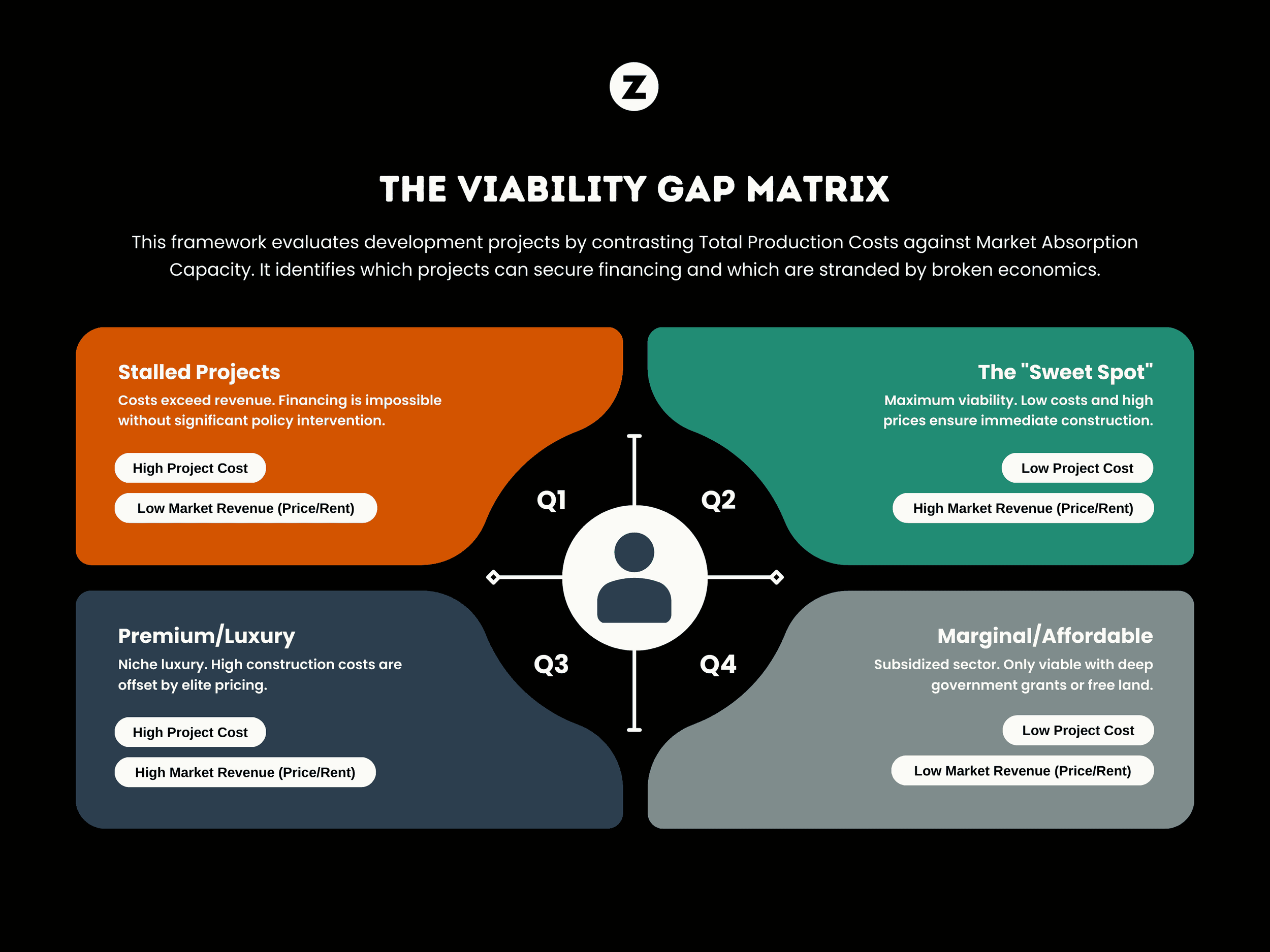

The Core Framework: The Viability Gap Matrix

To move forward, policymakers and developers must adopt a shared mental model for diagnosing the current impasse. We can visualize this using the "Viability Gap Matrix," a 2x2 framework that plots the relationship between Project Cost (Hard costs, soft costs, financing, and government charges) and Market Revenue (Achievable sale price or capitalized rental income).

Ontario’s Viability Gap Matrix

Quadrant 1: High Cost / Low Revenue (Stalled Projects) This is where an estimated 80% of potential Ontario housing projects currently reside. The costs to build exceed the price the market can bear. A developer may have the zoning for a 25-storey tower, but if the all-in cost per buildable square foot (PSF) is $950, and the achievable market price is only $1000 PSF, the margin is too thin to absorb the risk, secure financing, or generate the required Internal Rate of Return (IRR) (typically 15-18% for merchant builders). This quadrant is the graveyard of good intentions.

Quadrant 2: Low Cost / High Revenue (The "Sweet Spot") This is the elusive target for viable market-rate development. Projects here benefit from efficient construction methodologies, lower land basis, or streamlined government charges, while still commanding strong market rents or sale prices. Historically, this quadrant was occupied by high-density urban projects during periods of low interest rates and rapid price appreciation. Today, it is sparsely populated.

The Anatomy of the Gap

The transition of projects from Quadrant 2 to Quadrant 1 is directly attributable to the confluence of macroeconomic factors previously analyzed: specifically, the 40% escalation in costs paired with the concomitant 20% erosion of purchasing power.

The breakdown of costs reveals these pressure points:

Hard Cost Escalation: The cost of materials (steel, concrete) and, more critically, skilled labor (crane operators, formwork specialists) has made traditional cast-in-place concrete construction prohibitively expensive.

The Interest Carry Burden: In a high interest rate environment, time is the enemy of the pro-forma. Construction financing rates have moved from 3-4% to 8-10%+. A 36-month construction timeline for a high-rise tower incurs massive interest carry costs. Delays compound this burden exponentially.

The Government Levy Load: Development Charges (DCs), parkland dedication fees, Community Benefit Charges (CBCs, the evolution of Section 37), and HST collectively add $100,000 to $150,000+ to the cost of a new unit in many GTA municipalities. Crucially, these charges are typically levied upfront, crippling early-stage cash flow.

The objective of any effective housing strategy must be to mathematically shift projects back into Quadrant 2. This requires pulling specific, technical levers that directly address the components of the Viability Gap.

The "Unsexy" Solutions: Three Levers to Fix the Pro-Forma

Fixing the viability crisis does not require grand gestures or ideological battles. It requires pragmatic adjustments to the fiscal and operational framework of development. The solutions are not politically sexy, but they are mathematically sound.

Lever One

The single most impactful policy change the Provincial and Municipal governments could implement is a shift in the timing of government levies. The front-loading of Development Charges and the HST on construction costs has a devastating impact on a project's IRR due to the time value of money.

DCs are often due upon the issuance of building permits. HST is payable on construction inputs as they are incurred (even if later recovered via Input Tax Credits, the cash flow impact is significant). This increases the peak equity requirement for developers and inflates the interest carry in a high-rate environment.

The Proposal: A mandatory provincial policy that defers the payment of all municipal Development Charges, CBCs, and parkland fees until the point of occupancy or final closing (for condos). Furthermore, the province should coordinate the deferral of the provincial portion of the HST on development costs until the point of sale.

The Mathematical Impact: The impact on IRR is profound because IRR is highly sensitive to the timing of cash flows. By deferring significant costs (often 15-20% of the total project budget) from Year 1 to Year 3 or 4, the IRR increases substantially.

Consider a hypothetical 200-unit development with $20 million in DCs. Under the current system, this $20 million must be financed upfront. If the construction timeline is 3 years, and the cost of capital is 9%, the interest carry on these levies alone is approximately $5.4 million.

By deferring these payments until occupancy, we achieve several critical outcomes:

Improved IRR: Deferring costs significantly enhances the project's IRR - often by 200-300 basis points. This is frequently the difference between a viable project attracting capital and a stalled one.

Reduced Equity Requirement: Developers require less upfront capital (lower peak capital requirement), lowering the barrier to entry and reducing reliance on expensive mezzanine financing.

De-Risking the Project: It aligns the timing of government revenues with the realization of the project's value.

Addressing Municipal Concerns: Municipalities argue that DCs are necessary to fund infrastructure ("growth pays for growth"). This principle is valid, but the current timing is counterproductive. If the upfront cost of DCs prevents the growth from occurring, the municipality collects nothing.

To mitigate the impact on municipal cash flow, the Province must establish a revolving loan fund or "Infrastructure Bank" that provides low-cost financing to municipalities for growth-related infrastructure, backstopped by the future DC receivables.

This is not a tax cut; it is optimized financial engineering. It aligns the timing of government levies with the realization of revenue, fundamentally improving the financial viability of housing development.

Lever Two

The second lever addresses the structural inefficiencies of traditional construction methodologies. The construction industry is one of the least digitized, most inefficient sectors of the economy. While manufacturing has achieved massive productivity gains, construction productivity has remained flat. Ontario's reliance on bespoke, on-site construction is slow, labor-intensive, and wasteful.

The "Missing Middle", specifically targeting mid-rise, multi-family housing (4 to 12 storeys) is particularly challenging to deliver economically using traditional concrete forming methods, which have high fixed costs. If we are to address the 40% increase in hard costs, we must move from construction to assembly.

The Proposal: A concerted provincial effort to transition the construction industry from traditional on-site building to off-site manufacturing, specifically panelized systems and volumetric modular assembly.

Panelization: Walls, floors, and roof systems are manufactured in a climate-controlled factory and then rapidly assembled on-site.

Volumetric Modular: Entire units are built and finished in a factory, transported to the site, and stacked into place.

The Mathematical Impact: The 30% Time Reduction Target The primary benefit of industrialized construction is speed. By running the manufacturing process in parallel with site preparation and foundation work, we can realistically cut total project timelines by 30% or more. In development, speed is the new margin.

Reduced Construction Financing Costs: A shorter construction period means significantly lower interest carrying costs. If a 3-year project becomes a 2-year project, the savings on a $100 million construction loan at 9% can be $9 million.

Improved Labour Productivity: Off-site manufacturing utilizes labour more efficiently in a controlled environment, mitigating the impact of the skilled trade shortage and reducing cost overruns.

Faster Revenue Generation: Delivering units faster allows developers to recycle their capital into new projects more quickly, increasing the overall velocity of housing delivery.

Implementation Strategy: The Pre-Approved Catalogue

The primary barrier to scaling modular construction is the lack of standardized designs and the fragmentation of municipal approval processes. We must break the cycle of treating every building as a prototype.

Standardization of Design: The Ministry of Municipal Affairs and Housing (MMAH) should develop a catalogue of pre-approved, standardized designs for "Missing Middle" housing types optimized for manufacturing.

Automatic Approval: Crucially, projects adopting these designs should receive expedited approvals, cutting timelines from 12-18 months down to 90 days, bypassing the lengthy Site Plan Approval and Committee of Adjustment processes.

Manufacturing Investment Incentives: Providing significant tax incentives (e.g., accelerated Capital Cost Allowance) and low-interest loans for investment in automated housing manufacturing facilities within Ontario.

Moving from bespoke construction to industrialized assembly is the only scalable way to structurally reduce hard costs and bend the cost curve.

Lever Three

The shift towards Purpose-Built Rental (PBR) is essential, especially given the collapse of the condo market. PBR offers a stable, long-term yield that is attractive to institutional capital (pension funds, REITs). Programs like CMHC’s MLI Select are helpful, but attracting the massive amount of capital required demands stability and predictability of Net Operating Income (NOI).

In Ontario, the single greatest threat to NOI stability is the dysfunctional state of the Landlord and Tenant Board (LTB).

The Problem: 8-Month Eviction Lag The LTB is plagued by chronic delays. The current average delay for an LTB hearing for clear-cut non-payment of rent is approximately 8 months. This means a landlord must carry the operating costs (mortgage, property taxes, maintenance) for a unit with zero revenue for nearly a year before they can regain possession.

This regulatory failure introduces a significant risk premium into the PBR pro-forma. The "LTB Risk Premium" manifests as higher contingency budgets for bad debt and legal costs.

The Mathematical Impact: This increased risk profile deters the institutional capital necessary to build PBR at scale. Investors demand a higher capitalization rate (Cap Rate) to compensate for this operational risk. A 50-basis point increase in the Cap Rate (e.g., from 4.0% to 4.5%) due to perceived LTB risk can reduce the stabilized value of a project by millions, rendering it unviable.

By reducing the eviction lag, we significantly de-risk the investment, attract capital, and ultimately increase the supply of secure, professionally managed rental housing.

The Solution: Bill 60 and Targeted Action The Fighting Delays, Building Faster Act (Bill 60) provides the legislative framework for reforming administrative tribunals. This framework must be urgently applied to the LTB to create specialized, rapid adjudication streams for clear-cut cases. The goal must be to reduce the eviction timeline for non-payment from 8 months to 30-60 days.

The required reforms include:

Specialized Adjudicators: Appoint specialized adjudicators focused solely on non-payment issues (L1 applications), separate from more complex disputes.

Digital Transformation: Mandate digital filing and virtual hearings for non-payment cases, streamlining the administrative process and moving away from paper-based inefficiencies.

Mandatory Timelines: Implement statutory timelines for hearings and decisions for undisputed non-payment cases.

Reforming the LTB is not about eroding tenant protections against bad-faith actions; it is about ensuring the basic contractual obligation of rent payment is enforceable in a commercially reasonable timeframe.

The "War Story" (Case Study): A Stalled Condo in Mississauga

To illustrate the practical application of these concepts, consider a hypothetical case study representative of dozens of projects currently stalled across the GTHA.

The Project: "The Meridian," Mississauga City Centre

Initial Concept: A 200-unit high-rise condominium tower.

Zoning: Approved FSI of 6.0.

Timeline: Land acquired in 2022.

The Crisis: The Collapse of the Pre-Sale Model

The developer planned a pre-sale launch for mid-2024. By the time they launched, the market had shifted dramatically.

The Pro-Forma Crisis:

Cost Escalation: Construction hard costs had risen from an anticipated $400 PSF to $550 PSF. Financing costs had also doubled.

Revenue Compression: The required selling price to cover these escalated costs and soft costs ($100k/unit in DCs) exceeded $1,250 PSF. However, the market benchmark price had fallen to $1,050 PSF.

Viability Gap: $200 PSF.

The project was insolvent on paper. Furthermore, the lender required 70% pre-sales to secure construction financing. After six months of marketing, only 25% of the units were sold. The project was firmly stuck in Quadrant 1 (High Cost / Low Revenue) and faced cancellation.

The Pivot: Conversion to Purpose-Built Rental (PBR)

The developer recognized that while the condo market was soft, the rental market in Mississauga City Centre remained robust, driven by high immigration. Rental rates were achieving $4.50 PSF per month.

The pivot to PBR changed the economics. Instead of relying on upfront sales revenue, the project would be valued based on the capitalized Net Operating Income (NOI) upon stabilization. However, conventional financing still resulted in a low yield on cost.

The Solution: Leveraging CMHC "MLI Select"

The critical catalyst was the CMHC "MLI Select" program. This program provides significant financing advantages for PBR projects that meet certain affordability, accessibility, and energy efficiency criteria.

The MLI Select program offered several key advantages that fundamentally altered the pro-forma:

Extended Amortization: 50-year amortization (compared to 25 years for conventional loans). This dramatically reduced the annual debt service cost and improved the Debt Service Coverage Ratio (DSCR).

Higher Loan-to-Cost (LTC): Up to 95% LTC, drastically reducing the developer's equity requirement.

Favorable Interest Rates: Interest rates significantly lower than conventional construction financing, based on government bond yields (100-150 basis points lower).

Fiscal Incentives: The developer also benefited from the federal removal of the GST/HST on PBR construction (a significant cost saving).

The Outcome: A Viable Project (Moving toward Quadrant 2)

By pivoting to PBR and utilizing the MLI Select program, the developer was able to secure financing and commence construction. The reduced debt service costs and lower equity requirement made the project attractive to institutional investors.

The "Meridian" case study demonstrates that viability is not static. It can be achieved through strategic pivots that align the project with the available financing tools and policy incentives. However, this pivot relies heavily on federal programs. If the provincial levers discussed earlier were also implemented - DC deferral (Lever 1), faster construction (Lever 2), and LTB reform (Lever 3) - the project's viability would be significantly enhanced, and more projects like it could proceed.

Conclusion: The Mathematics of Momentum

The Ontario housing crisis is fundamentally a mathematical problem. The inputs (costs) exceed the outputs (revenue). Continuing to focus solely on zoning and approvals while ignoring the financial viability of development is an exercise in futility.

The market is clearly signaling that the current framework is broken. We must move beyond the "Supply Myth" and address the "Viability Gap." The three levers outlined above provide a technical roadmap for achieving this objective.

These are not ideological proposals; they are pragmatic solutions grounded in the mathematics of development. They address the core components of the pro-forma: cash flow, cost, and risk.

The following is a "Monday Morning Checklist" for the Ministry of Municipal Affairs and Housing (MMAH); a pragmatic, actionable roadmap to restart housing starts in Ontario.

Checklist for the Ministry of Municipal Affairs and Housing

1. Implement Immediate Fiscal Reform (The Tax Shift):

Action Item 1: Introduce legislation amending the Development Charges Act and the Planning Act to mandate the deferral of all municipal DCs, Parkland Levies, and CBCs until occupancy for all residential developments, regardless of tenure (condo or rental).

Action Item 2: Engage with the Ministry of Finance to coordinate the deferral of the provincial portion of the HST on new construction until the point of sale/occupancy.

Action Item 3: Develop a plan to establish a provincial Infrastructure Bank or revolving loan fund to provide interim financing to municipalities for growth-related infrastructure, backstopped by future DC receivables.

2. Catalyze the Construction Productivity Revolution (Construction Tech):

Action Item 4: Launch the "Missing Middle Design Catalogue" initiative. Develop a library of pre-approved, standardized designs for multiplexes and mid-rise housing (4-12 stories) optimized for manufacturing (panelized, modular, mass timber).

Action Item 5: Announce a 90-day expedited approval pathway (bypassing Site Plan Approval and Committee of Adjustment variance processes) for projects utilizing these pre-approved designs.

Action Item 6: Collaborate with the Ministry of Economic Development to introduce investment tax credits (including accelerated CCA) and low-interest financing for scaling up off-site manufacturing capacity in Ontario.

3. Restore Functionality to the Rental Market (LTB Reform):

Action Item 7: Direct the Attorney General to immediately implement the administrative reform provisions of Bill 60 focused on the LTB.

Action Item 8: Launch an emergency intervention with the explicit goal of reducing the average adjudication time for clear-cut non-payment of rent (L1 applications) from 8 months to 60 days.

Action Item 9: Implement a surge hiring of specialized adjudicators and mandate a fully digitized case management system (Digital-First Adjudication).

These levers are not politically expedient, nor do they lend themselves to easy slogans. They are technical, rigorous adjustments to the machinery of housing delivery. The time for political theatre is over. It is time to do the math.

Resources

Fall 2025 Housing Supply Report

Ontario housing projections plummet again, hurting 1.5M goal

Further Reading

Southern Ontario’s Home Affordability Crisis Remains at Near-Record Levels

Barriers to Housing Supply in Ontario and the Greater Toronto Area

Uba Abraham

The visionary founder of Zulma Real Estate, established in 2023.

Recognizing the need for a more proactive approach to asset stewardship and the common decline in long-term property value, Uba launched Zulma Real Estate with a focused and measurable goal: to provide superior property management that secures and prolongs the long-term value of every investment. The firm is committed to partnering with 5,000 homeowners and investors to ensure their assets appreciate over time by 2030.

Uba and the Zulma team are dedicated to maximizing your real estate investment's enduring success through expert management and preservation.

Join Zulma Community. Connect, Share, Grow!

- Get fast answers in active discussion forums

- Join or create a club and grow your investor network

- Access free calculators and essential investor resources

- Discuss industry news and insights with like-minded peers